Ep # 91: What History Tells Us To Expect From Investments In 2023

Nobody wants to relive the results of last year from a market perspective. But, we can use this historical context as a guide to shape our outlook for 2023. The odds of us having a positive year this year are in our favor, even though we are still facing many of the same issues.

Ben and Adam hope that giving some historical context will help investors understand what to expect from investments this year.

- (2:05) Understanding the current market environment

- (3:52) What are the odds that a positive year is followed by a negative year? Or a negative year followed by another negative year? Or a negative year followed by a positive year?

- (6:54) The importance of diversification in the market

- (8:22) The worst performance of bonds since 2008

- (10:03) The Federal Reserve's interest rate environment

- (11:15) Preparing for a recession

- (15:53) The positives

Source: FactSet, Standard & Poor’s, Robert Shiller, Yale University, Bloomberg, Ibbotson/Strategas, J.P. Morgan Asset Management.

The 60/40 portfolio is 60% invested in S&P 500 Total Return Index and 40% invested in Bloomberg U.S. Aggregate Total Return Index. S&P 500 returns from 1950 – 1970 are estimated using the Shiller S&P Composite. U.S. fixed income total returns from 1950 – 1975 are estimated using data from Strategas/Ibbotson. The portfolio is rebalanced annually. Guide to the Markets – U.S. Data are as of December 31, 2022.

Watch the full video on YouTube:

Full Transcript:

Benjamin Haas 00:03

Hi everyone and welcome to A/B Conversations, where we will help you CFP your way out of it. A podcast where you get into the minds of a couple of Certified Financial Planners on how we think and feel about everyday financial planning questions and what should really matter most to you. A healthier financial life starts...now!

Adam Werner 00:25

Hey Ben. Welcome back to the podcast, once again.

Benjamin Haas 00:28

I am pleased to be with you, my friend, looking forward to enlightening whoever to listen to us or I hope it will be enlightening.

Adam Werner 00:38

I think that should just be a regular motto of ours. Just I hope this is enlightening to whoever listens to it. And if that's

Benjamin Haas 00:47

There you go.

Adam Werner 00:48

20 people, fantastic. If that's 1000 people, I don't think that's ever going to be the case. But that's ok.

Benjamin Haas 00:56

That's right. That's right.

Adam Werner 00:58

For the people that it matters to, that's where we want to speak to. So, on that note, today's podcast is a topic we haven't covered in a little bit - investments. We often think people understand they work with a financial advisor and investments are a huge component of that for many people. It's the only component to that. I think we very clearly have a different approach to our jobs being planners first, investments being secondary, but it doesn't make the investment side of things any less important. I think we have a different or maybe I shouldn't say that, we have a unique approach in our minds, like our philosophy is pretty fundamental. We're not out there, you know, selling on performance, and hey, you have to work with us because our investments are just so much better than anybody else's. Sorry, all of that to say, today's purpose. I don't know how I got off that sidetrack there. Today's purpose is, no one wants (your words), no one wants to relive the results of last year from a market perspective. But there is some history there that we can use as a guide to put into context, last year's returns, and kind of our outlook for 2023.

Benjamin Haas 02:18

There you go, so you hit the two words that I was really focused on to get this kick started. It is context, both as financial planners but also as professionals here that do need to work with people that emotionally felt pretty crappy about last year. Let's call a spade a spade and also to kind of be forward looking. So I like the way you frame that up. I'll pass it back to you; I think looking at history. I know there's always going to be this argument of well, history doesn't repeat itself. Yeah, I get that. But it often does rhyme. I think there is important context, looking back on how did last year compare to what has been kind of expected of portfolios over time and returns over time at different asset classes, and allow that to kind of paint a picture for us on how we move forward.

Adam Werner 03:09

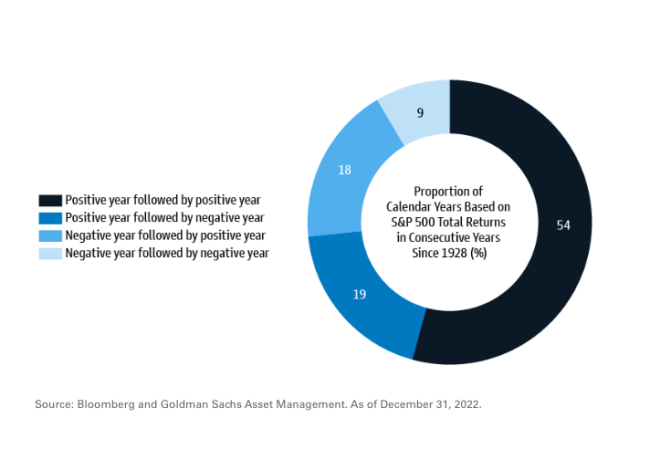

Yeah, so I think most of the people that work with us know, we do a lot of reading, we hear a lot. We're tuned in on the investment side because that's part of our job. And one of the, I don't know if it was a blog post or an article, doesn't matter, but it was from Goldman Sachs. It was a nice little pie chart that just broke down historical returns into four different categories and it really was just focused on what happened the previous year, can potentially dictate what happens the following year, and its calendar year returns. Meaning, if 2022 was a positive year, what are the odds that 2023 was also a positive year for market performance?

Benjamin Haas 03:51

54%?

Adam Werner 03:52

Thank you. So yeah, we can kind of go through that but then it's what are the odds that a positive year is followed by a negative year. A negative year followed by another negative year or a negative year followed by a positive year. So obviously, we're focused on the hey, 2020 was a negative year for pretty much all investments, stocks and bonds together down the for the first time in quite a while. But statistically speaking, a negative year followed by a negative year only happens 9% of the time, historically speaking, 9%. So, that includes all of the positive returns, followed by positive returns. But even in the consequent context of looking at last year being a negative year, two thirds of the time this following year, 2023, in this instance, is positive, or has been positive in the past. So not saying that 2023 we think is, hey, we're going to erase the pain of last year and we're all going to feel good at the end of 2023. I don't necessarily believe that's the case. We can go into a little bit of those details as to maybe why, but statistically speaking, the fact that we are starting at a much lower point than where we were to start the year last year. It's all about that starting value. So, I don't want to say there's only one direction we can go from here because that's not true. But the odds of us having a positive year this year are in our favor.

Benjamin Haas 05:16

So, I think that's really important because I don't know, you and I haven't talked about this. So now I'm kind of like riffing here with you. But it always seems to me that after a negative year, now I'm going back to 2018, that we get these phone calls from complete strangers. Not people that we work with, right at the beginning of the year going, I have to go, I have to do something different. It's like that annual statement kind of triggers something in somebody and while that's great, we're here to help people, here to coach them through that what you just shared is really important to recognize. The market goes up more than it goes down. It never feels good when it goes down and we'll talk about this a little bit later. You probably will feel bad for a little while here while the market maybe even is going up. That's just psychologically kind of how it works. I love that stat because it really puts it into perspective of the odds are actually pretty low, 9%, that we would have a negative year followed by a negative year. That's it. So, I mean, if you know nothing about markets, hang in there and recognize that odds are in your favor that the worst is behind you.

Adam Werner 06:24

Yeah, there's always the saying that there's always the exception that proves the rule. Right, which I'm not exactly sure how that thing works but last year's results do impact us moving forward. So yeah, I guess we'll kind of see where this year ends up. But yes, statistically speaking, this year shouldn't be another down year but we'll see what happens.

Benjamin Haas 06:51

Yeah, and maybe we'll make a quick pivot here because I think we often use these statistics and what we read and what people turn on into the news, when you say the market, we really are talking about stocks. As financial planners, it really is our job for the vast majority of our clients to diversify and that includes bonds. So, without going into the deep and dirty details of interest rates really going up last year and inflation being a problem. Hence, bonds having a very negative return. Let's maybe shift to just talking about diversification.

Adam Werner 07:25

So I know, we've said this on many different podcasts, or maybe not many. But for 2022, diversification did not work. To your point, stocks were down, bonds were down and I think we've been trained and I think investors, clients have been kind of trained over the years that we were going to own a little bit in each. We're going to own some stocks, we're going to own some bonds so that when the stock market is in trouble, that our bonds are going to hold their value or maybe even increase in value because there's going to be a flight to quality. These things are going to zig when the others are zagging and it's all going to smooth things out in the end and that is mostly true. Last year did not bear that out so I think that also put a little bit more pressure from an investor standpoint of, well, I'm diversified, but everything's down. So now really, what? But yeah, so that 60/40 portfolio in this instance, we're going to exclude kind of international investments, we're purely just thinking the S&P 500 in the US, and the Barclay’s aggregate bond index, again, being US-based. This was the worst performance that we've seen since 2008. Which, for anybody listening, go back and remember or look at what happened in 2008. It was also the first year since 1974, that both stocks and bonds were negative in the same calendar year together. So, we're going back almost 50 years since we had a market return environment like we did last year, which is kind of crazy to think about. 50 years.

Benjamin Haas 09:08

Yeah, and at some point, again, I think we just need to move people's attention to okay, then what typically follows that, these asset classes and the market. If the market is not the economy, right, we're going to hear a lot of economic reports and are we going into recession? Are we not? It is intended to be a forward-looking thing, right? So, we can look at all that and go, oh my God, it was historically bad. And even hearing that, while it was happening, I couldn't grasp that. I couldn't really grasp how this environment that we're in in 2022 is like, historically bad. You expect that in a pandemic. You expect that like Great Depression, right? These are huge, horrible events. But you look past that, you look at how diversification has performed in the years following that and it's going to be a pretty similar story right?

Adam Werner 10:00

Yeah, so that I guess that's a great segway. You set me up for this perfectly. A lot of the issues that we were facing last year in the markets, they haven't gone away. They're still present this year. It's what is the Federal Reserve going to do? It's inflation. It's the economy, we know things are slowing down, we're starting to see those reports. So, a lot of that hasn't necessarily been solved but the trend is now finally pointing in the right direction. Inflation seems to have peaked at some point last year, we're getting those data points that are pointing us in the right direction. We're hoping that that also then leads to the Federal Reserve, starting their change in policy to point us back in the right direction. So going back last year, being negative for both stocks and bonds, one of the big drivers there was the Federal Reserve, interest rate policy, inflation, and both stocks and bonds are affected by the interest rate environment. For better or for worse, that's kind of what drove things last year. So, in thinking for this year, we may, we may not see a recession. At this point, I don't want to say it doesn't matter but in terms of

Benjamin Haas 11:19

I was going to use those words.

Adam Werner 11:21

Yeah, in terms of the market, like you said earlier, it's a lot of future events have to get priced into today. To your point of things being very for the market being very forward looking. This may be the most anticipated recession, if we get one that we've seen. So, there's a lot of reasons why it should then feel like more of a nonevent, if it all kind of plays out the way the experts and a lot of the commentary that we're reading kind of expect. That if we do see a recession, these big businesses are kind of prepared for it more so than when it's a shock to the system, or just a bigger, a bigger. I don't know. My words are failing me here. But a surprise,

Benjamin Haas 12:06

It's a Monday.

Adam Werner 12:07

That kind of a surprise. You're pulling back the curtain we usually record these on Fridays. A bigger surprise to the system that now it feels like COVID shutdown happens. Now, how do we navigate this environment and thinking like, you know, these massive multinational companies. This has been coming for a really long time. So in theory, even if we do have a recession, it should be relatively short lived, it should be relatively shallow, and in the eyes of the market, then we're probably going to be feeling pretty negative, even while the market is probably starting to turn the corner and rebound before we are kind of ready or understanding how is this happening?

Benjamin Haas 12:51

Just goes back to human nature. We live in the day by day, we read headlines. We're living in the moment but as long-term investors, especially as advisors, wealth managers here trying to advise people to be long term investors. When would you want to do buying? When would you want to like grab something that you feel like is going to appreciate over long periods of time? Are we trying to time the bottom? No. But that's why I think the market really is trying to do that for us in a way of going, well it doesn't matter if today's the bottom or June's the bottom. Where do we project things? And where do we see things going in the business cycle? The economic cycle will improve at some point. I don't know if it's this year or not but historically speaking, the market is not waiting for that news to kind of like, all right, coast is clear, everybody. That's not it. We're probably, historically speaking, statistically speaking, we're going to see some of that recovery, as you said, just because we're trending towards that not yet.

Adam Werner 13:55

And this just popped into my head, but you know, there is the wisdom of crowds and that's not the right terminology, but like the wisdom of the crowd. The one that always sticks out in my head is, you go to the county fair, there's this jar of jelly beans and you have to guess how many are in it. And there's been studies on this that any one person's guess, like your odds of getting close to the number are very, very low. But when you take everybody's guesses and average them out, it's really darn close to what the actual number is in the jar. You get enough people inputting kind of their guess and the average is usually pretty darn close to the actual answer. I think the stock market is a lot like that where you have the people that may be more optimistic. You have the people that are more pessimistic. You throw all of that into a blender, you spit it out the other side and where is there more people? Leaning to the optimist side or to the pessimist side, and that's where you can kind of see the momentum in the markets. I think last year was definitely a big part of that where some selling or some negative news just began more negative and more negative, it's a self-perpetuating cycle at a certain point. I don't know that we're necessarily beyond that. I certainly would not be shocked if we do see a lot of volatility here over the first, I don't know, three to six months until we get a much clearer picture on what the Federal Reserve is going to do. But beyond that, I think we are in store for some positive returns. Again, I don't think we're just going to magically rebound and hit all-time highs just like that. But I think 2023 is a pivotal year to at least take some of the pressure off of investors feeling the negative and at least hopefully, by the end of the year, you get some type of return that doesn't have a you know, a minus sign in front of it.

Benjamin Haas 15:53

I'll say one more thing to that and then I think I'm done with the points that I would have wanted to make today. It's not just to look for the silver lining here. Again, I hope I sounded actually a little more optimistic than that but I know you and I have talked to clients a lot about this. One of the positives of interest rates going up is that this whole idea of the 60/40 portfolio, hey, it didn't work, bonds didn't hold up last year. Well, at least they're yielding now. Something that feels far more attractive for us. Where if you think about how you go about making money, especially if we're talking to retirees, but that 60/40 portfolio, we want it producing income. You're living off of that. So even if the value is going down that income, as long as we're not buying and selling those values going down or up, that income should be increasing. We're now talking to people about 3% and 4%. CDs. I feel like we haven't done that in the last 10 years. It is to kind of lean into, well, that horrible reset, you know, that ripping of the band-aid that felt so bad. There are some positives, even if it's not this year and even if it's not the market fully recovering, like you said, there are positive to this whole idea of how am I going about my retirement planning? How am I recreating my paychecks now, five years from now? Do I need to do something vastly different? I don't think you do, generally speaking and I hope more income clearly than means taking the pressure off of capital appreciation too.

Adam Werner 17:24

Yeah, it is interesting with that kind of as the perspective that for someone that is retiring, and is relying on their savings to essentially recreate their paycheck, in theory, if your portfolio is able to generate a higher level of income than it did a year ago, in theory, you need less money to generate the essentially that same level of income. So just from that standpoint, it's weird to kind of think through that lens of okay, well, if I needed a million dollars to generate $40,000. But now I only need like $800,000 to generate that same $40,000 I don't know, it just it puts into perspective, kind of the moving variables for investments, portfolios, and at the end of the day, for most people, it really is if when I get to retirement, I just I just need to recreate my paycheck, make sure that I have the income that I need to live the life that I want to live. And yeah, the markets, bonds and stocks, the dynamic has certainly shifted for 2023 because of everything that we experienced in 2022 and we'll see where things end up. But the fact that we experienced all of that pain should at least set us up for some positive. It's just a matter of when, not if.

Benjamin Haas 18:46

Well said. Goes back to the original comments. It's context and perspective so I hope we gave a little bit of both today.

Adam Werner 18:54

Yeah, and if anybody has questions who wants to talk through it, what it actually means for them and their situation, let us know. Happy to go through it.

Benjamin Haas 19:03

Here's to a better 2023!

Adam Werner 19:06

Cheers to that.

Benjamin Haas 19:07

Thanks pal.

Adam Werner 19:08

I'll see you next time.

Benjamin Haas 19:09

See you soon. Hey everyone, Adam and I really appreciate you tuning in. Please note that the opinions we voiced in the show are for general information only and are not intended to provide specific recommendations for any individual. To determine which strategies or investments may be most appropriate for you, consult with your attorney, your accountant and financial advisor or tax advisor prior to making any decisions or investments. Thanks for listening!

Tracking # T005302